|

Betty Tessien

Most the major producers of flow and treat equipment and services are headquartered in developed countries. The major exception is China. Domestic companies such as Neway have become international producers. Neway is supplying high performance valves for critical applications around the world. The big growth markets are in India and other Asian countries along with Africa. The challenge for international suppliers relying on the U.S. market is to adjust to the new reality and capture a higher market share than they have in China.

The U.S. has an advantage which is likely to be temporary. It is the largest combined producer of oil and natural gas. This not due to having the largest reserves but to the American technology which perfected hydraulic fracturing. The flow and treat industry benefited with purchases for extraction, gas processing, transmission, refining and petrochemical expansions.

The problem is that China has more potential in shale oil and gas than the U.S. Other countries such as Argentina are moving forward to develop shale potential. The economies of China and India are growing faster than the U.S. Their combined population is more than six times that of the U.S. When their per capita GDP reaches just half of that in the U.S. their GDP will be three times that of the U.S.

Africa will experience economic growth as will developing countries in Asia and elsewhere in the world. As a result, flow and treat purchases in the U.S. are likely to drop from an 11 percent share in 2020 to an 8 percent share in 2030.

The biggest loss of share will be in municipal wastewater. The U.S. has been slow to invest in infrastructure whereas the rest of the world is investing in treatment facilities which in some cases will exceed the quality of those in the U.S.

The developing countries will continue to invest in coal fired power over the next ten years. China is upgrading its plants so that they will be as clean as natural gas combined cycle generators. The expenditure for flow and treat products per MW of coal fired power is more than 40 times that for wind or solar. As a result, the U.S. power plant flow and treat revenues will represent just 8 percent of the total in 2030.

The U.S. will benefit from the rapid growth of the biopharmaceutical industry. Even though the world market share percent will drop the year to year growth will be significant. However, the trend is away from stainless steel products to those made from polymers for single use. Semiconductor and flat panel display manufacturing will continue to grow in Asia. The U.S. mining flow and treat market share will drop from 10 percent to just 5 percent as both coal and iron ore production fall.

The food industry has been a strong market for U.S. flow and treat manufacturers. However, food processors are moving to where the people are. Raw materials such as palm oil will continue to gain market share over other vegetable oils grown in the U.S. cane will be a greater source of sugar than beets. The economics continue to favor sugar cane as ways have been found to produce ethanol from the bagasse as well as from the sugar itself.

Flow and treat suppliers have to devise strategies around the slower growth in the U.S. market compared to the rest of the world. Many of the purchasers such as BASF and Arcelor Mittal are international companies. They will increasingly centralize purchasing for plants around the world. Fortunately, for U.S. based suppliers, many of the international purchasers are home based in the U.S. This includes, food, oil and gas, and chemical companies.

Sales strategies centered around companies rather than geographies will be more cost effective. The development of products which have lower total cost of ownership will be desirable in order to meet local competition in the rest of the world. The initiative underway at Power-Gen this week is an example of how companies can validate lowest true cost to local purchasers.

Power-Gen and the Most Profitable Markets

Power-Gen International (November 18-21 in New Orleans) will include lots of flow and treat activity. There are a number of pump, valve, instrumentation and pollution control stands and relevant speeches. A new feature is the personal meeting program which helps set up meetings between individuals.

The McIlvaine Company assists suppliers with the Most Profitable Market Program www.mcilvainecompany.com. This includes quantifying applications where the supplier has the lowest true cost and can therefore generate the most profit. As a result, McIlvaine is working with conference organizers, associations, media, end users and others on True Cost Investigations.

This effort is continuous. The true cost data gathered for the Dry Scrubber Users Group, INDA, the association of non-woven producers, or Mission Energy (representing Indian power plants) is then made available and expanded at exhibitions such as Power-Gen. Much of the data is linked to articles in magazines such as Power Engineering. One magazine, International Filtration News, is taking a proactive approach with True Cost Investigations as feature articles in each issue. This can be expanded with true cost webinars for direct validation of cost claims.

McIlvaine was a scheduled speaker at the Power-Gen workshop on the 18th relative to helping companies pursue the international market. The workshop was canceled due to low registration. On the other hand, there are Power-Gen events all over the world where access will be available to international suppliers through True Cost Investigations.

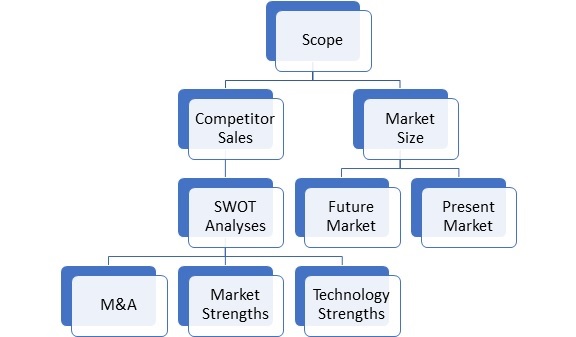

The Most Profitable Market is not only one where the supplier has competitive true costs but where he can validate them. Exhibitions such as Power-Gen and magazines such as Power Engineering are vehicles for reaching the purchasers and communicating the true costs. The investigations become some of the evidence needed for the effort. The available Investigations for Power-Gen include:

Updates: Contact information and arrangements are being continuously revised. So, keep checking this document.

Overview: This provides the schedule of speeches, details on relevant exhibitors, and contacts for relevant personnel.

Electrostatic Precipitator Power Supplies True Cost Investigation

Gas Turbine Inlet Filter True Cost Investigation

Turbine Bypass Valve True Cost Investigation

Dry Scrubbing True Cost Investigation

CCR True Cost Investigation

FGD Recycle Pumps

Improving Limestone Scrubber Efficiency

This Power-Gen initiative is part of a collaborative program.

The program is a collaborative effort involving associations, media, suppliers, consultants and the power plant operators.

|

Effort

|

McIlvaine

|

Magazines

|

Conferences

|

Associations

|

Supplier

|

|

True Cost Investigation

|

|

x

|

x

|

x

|

x

|

|

Most Profitable Market Forecast

|

x

|

|

|

|

x

|

|

Lowest True Cost Claims

|

|

|

|

|

x

|

|

Indirect Validation

|

|

x

|

|

|

x

|

|

Direct Validation

|

|

|

x

|

x

|

x

|

Suppliers use the true cost validation and most profitable market forecast to initiate a sales program which will validate their claims of lowest true cost and result in high margin sales. From the customer perspective the payment of the higher product prices is more than offset by life cycle cost reductions and more efficient operations.

Bob McIlvaine can answer questions prior to and during the show. You can reach him by cell phone at 847 226 2391 or email rmcilvaine@mcilvainecompany.com.

Activities at the show are updated continually at http://www.mcilvainecompany.com/PowerGen_2019/MPM/powergen_and_the_most_profitable.htm

Click here to un-subscribe from this mailing list

|