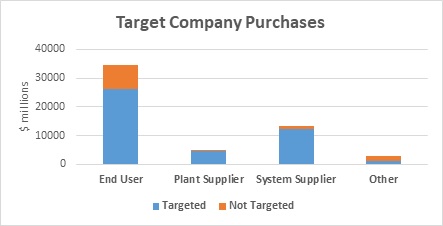

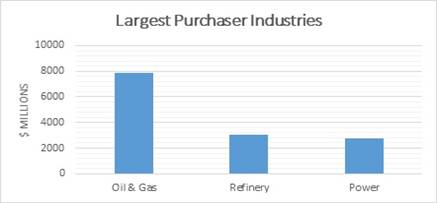

Seventy-One OEM/EPC Contractors Spend More Than $9 Billion For Valves

A small number of companies purchase a large percentage of industrial valves.

The McIlvaine company in

Industrial Valves: World Market

identifies these companies and provides estimates of their yearly valve

purchases.

The largest OEMS and EPCs account for more than 15 percent of the valve

purchases. Of this total 4 percent is sold to the largest end users and 11

percent to smaller end users. The largest end users and OEM/EPCs combine

for 34 percent of the total valve purchases. When additional purchase

influenced by the top 20 design firms are included the total is 40 percent of

all purchases.

Seventy-one OEM/EPCs spend $8690 million for valves for an average of $122

million each. Eight OEM/EPC companies supplying refinery systems account for

valve purchases of $2.3 billion.

The largest oil and gas contractors are

1.

Bechtel (USA)

2.

Technip (France)

3.

Aker Solutions (Norway)

4.

Chiyoda Corporation (Japan)

5.

SNC-Lavalin Group (Canada)

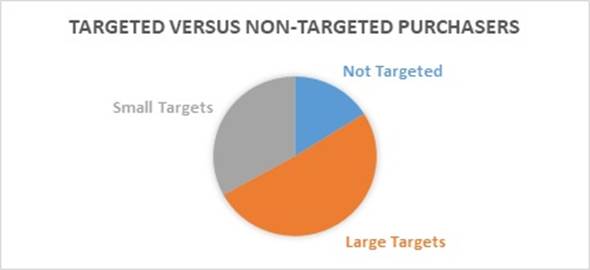

Valve sales people who are covering the 90 largest users, the 71 largest EPCs

and OEMs and the 20 largest design firms will be assured that they are pursuing

40 percent of the entire valve market. For more information on

N028 Industrial Valves: World Market,

click on:

http://home.mcilvainecompany.com/index.php/markets/2-uncategorised/115-n028.

This service provides detailed forecasts which allow the subscriber to determine

how much each of the major end users will spend in the coming year. It is even

possible to determine individual project potential with the 41F Utility

E-Alert:

http://home.mcilvainecompany.com/index.php/databases/28-energy/485-41fi

and the Oil, Gas, Shale, Refining E-Alert:

http://home.mcilvainecompany.com/index.php/databases/28-energy/991-71ei.

Liquid Filtration Market Will Be Slowed By Sinking Chinese Economy, Drop in Oil

Prices and New Technology

The liquid filtration and elements market will grow by 15 percent through

2019 predicts the McIlvaine Company in N006

Liquid Filtration and Media World Markets.

This forecast is predicated on oil prices of $80/barrel, a Chinese economic

growth of 7 percent and modest penetration of the market from competing

technologies. At $40/barrel oil, 2 percent economic growth in China and

greater penetration of competing technologies, the growth over the next four

years could be as low as 8 percent.

Oil prices, the Chinese economy and technology competition are three of the

biggest variables in the future forecasts. In order to understand the

impact on the total market one has to analyze each product type included in the

report.

|

Subject |

Market

% |

%

consumables |

Oil

impact |

China

impact |

Technology |

|

ABW Filter |

12 |

10 |

m |

m |

+ |

|

Bag Filter |

14 |

90 |

l |

m |

- |

|

Belt Filter Press |

10 |

40 |

l |

l |

- |

|

Drum & Disk |

10 |

40 |

l |

m |

- |

|

Filter Press |

15 |

60 |

l |

m |

- |

|

Granular Media Filter |

25 |

10 |

l |

m |

- |

|

Leaf, Tubular & Belt |

14 |

30 |

m |

m |

- |

Automatic backwash filters (ABW) represent 12 percent of the market. They

are used in oil and gas production. China is a significant purchaser.

This technology is gaining market share over cartridges (covered in a separate

McIlvaine report). This increased penetration is included in the present

forecast as indicated by the + in the table. Only 10 percent of the market is

consumables, so ABW filters are more vulnerable to economic swings than

are bag filters where 90 percent of the market is consumables.

The forecast already takes into account the lower market share for the other

technologies. McIlvaine anticipates that membranes will continue to carve out a

bigger share of the food market at the expense of leaf and disk filters. Under a

tough competition scenario, the market would be reduced even further.

Oil prices impact those product segments where the oil and gas industry is a

major purchaser. Some products e.g. belt filter presses, are sold

primarily to sewage treatment plants and are not going to be impacted by

changing oil prices.

There are many variables affecting the market. The Fukushima disaster

alone accounted for a 1 percent increase in the market for a period of two

years. The variables need to be continually evaluated. As a result,

McIlvaine is updating its forecasts on a quarterly basis.

For more information on

N006 Liquid Filtration and Media World Markets,

click on:

http://home.mcilvainecompany.com/index.php/markets/2-uncategorised/118-n006

Utility E Alert Tracks Big Opportunities Around The World

New power plants and large retrofit initiatives at existing plants generate very

large revenues for flow control and treatment suppliers relative to water

intake, coding, boiler feedwater and wastewater treatment. These are

tracked weekly in the Utility E Alert. Managers and sales people will

benefit greatly from this Alert which is only $950/yr. Here are some of

the headlines in the issue last week:

§

Two States' Regulators oppose Patriot Coal Reorganization Plan

§

Duke Energy to pay $975K Penalty plus do Environmental Work

§

NBET signs $5 Billion Agreement on 1200 MW Coal-fired Power Project

§

Two Japanese Firms shortlisted for Matarbari, Bangladesh Coal-fired Power Plant

§

Toshiba wins EPC Contract for Harduganj Ultra-supercritical Power Project in

India

§

Petrovietnam selects GE’s High-efficiency Steam Turbines for New Coal-fired

Power Plant

§

Tanjung Jati B plans 2 x 1000 Coal-fired Power Plants as Third Phase

§

Proposed AELs for Coal-fired Power Plants in Europe Would Tighten NOx

Permit Limits

§

Siemens to supply Equipment for 775 MW Keys Energy Center in Maryland

§

Combined Cycle Power Plant under consideration by Guam Power Authority

§

AES awarded Panama’s First Natural Gas-fired Power Plant

§

DOE selects Eight Projects to receive funding for reducing Cost of CO2

Capture and Compression

The alert has important water related information on projects. For

example:

Toshiba wins EPC Contract for Harduganj Ultra-supercritical Power Project in

India

Toshiba Corp.

announced that its Chennai, India unit Toshiba JSW Power Systems Private

Ltd. has been awarded a full EPC contract by Uttar Pradesh Rajya

Vidyut Utpadan Nigam Ltd or UPRVUNL in Lucknow, India. The value of the

contract is about $540 million. Toshiba JSW will carry out the engineering,

procurement, construction or EPC of the entire thermal power plant, including

civil and boiler island package to be completed within 48 months from the

contract award. Toshiba JSW will start delivering main equipment from October

2017, and the plant is expected to start its operation in September, 2019.

§

Water requirement for the proposed expansion will be 2,440 m3/hr. (24

cusec) with ash water re-circulation system.

§

Monitoring of surface water quantity and quality shall also be regularly

conducted and records shall be maintained. The monitored data shall be submitted

to the Ministry regularly.

§

Wastewater generated from the plant shall be treated before recycling/re-use to

comply with the limits prescribed by the SPCB/CPCB.

§

Flyash shall be collected in dry form and storage facilities (silos) shall be

provided. Unutilized flyash shall be disposed of in the ash pond in the form of

slurry. Mercury and other heavy metals (As, Hg, Cr, Pb, etc.) will be monitored

in the bottom ash and also in the effluents emanating from the existing ash

pond. No ash shall be disposed of in low lying area. Flyash shall be transported

by road through closed trucks only.

§

The ash pond shall be lined with HDPE/LDPE lining or any other suitable

impermeable media such that no leachate takes place at any point in time.

§

Space for FGD shall be provided for future installation as may be required.

For more information on the Utility E Alert, click on:

41F

Utility E-Alert

“Power Plant Water Monitoring” is the Hot Topic Hour on September 24, 2015 at

10:00 a.m. CST

A webinar on September 24 at 10:00 a.m. central time will cover the options and

issues regarding selection of fossil-fired plant water monitoring systems and

instruments. There is a very ambitious goal to provide a website with the

most comprehensive information on power plant monitors. This is part of a

whole knowledge system to provide Alerts, Answers, Analysis and Advancement in

every aspect of power. Owners and operators around the world have free

access to

44I Power

Plant Air Quality Decisions (Power

Plant Decisions Orchard) and

59D Gas

Turbine and Combined Cycle Decisions.

The Power Plant Water Monitoring Decision Guide is one of the subsidiary

websites in both these knowledge systems.

This webinar will be focused on creating a Power Plant Water Monitoring Route

Map and Summary which will help decision makers navigate the website. The first

inputs to this Route Map are displayed at Power

Plant Water Monitoring Route Map.

There is still time for vendors to submit one or two slides for the display

deck. We intend to discuss issues during the session but due to the 90 minute

limit most of the time will be just spent on determining which types of

monitors are best suited for specific applications.

The website already exists with presentations, articles and recordings. This

discussion will be followed by a continuing flow of additions to the system.

This webinar is free of charge. For more information on supplying data or

participating contact Bob McIlvaine at

rmcilvaine@mcilvainecompany.com.

Pump Market Forecast Changes Webinar - September 25, 2015

This 40 minute webinar will review changes to the forecasts in Pumps: World

Market. Explanations will be given for key factor selections such as

oil prices and Chinese economic growth. Examples of the type of information to

be presented are shown below

The pump industry will grow by 17 percent from 2015 to 2019 at oil prices of

$80/barrel during the period. At $40/barrel, the growth will only be 3

percent.

There are a number of variables which will determine the market growth for

pumps. New insights are continually generated which justify changes in the

forecasts. The Iran nuclear agreement is just one example. The plunging

economy in China is another. However, the most significant development recently

is the plunge in oil prices to $40/barrel.

The industrial pump market is dominated by oil and gas which represents 24

percent of the present market. However water and wastewater, power,

refining, petrochemical and other industries account for 76 percent of the

market. The impact of future oil prices on the market can be best

predicted by estimating the impact on the individual segments.

Oil and gas can be divided into two segments. The aftermarket and routine

purchases for small projects represent two-thirds of the total or 16 percent of

the present total pump market. The longer term large project revenues

represent only 8 percent of the current market. If the price of oil were

to continue to remain at $40/barrel through 2019, revenues in this segment would

shrink over the period.

At $40/barrel oil the long range pump product revenue from the oil and gas large

project segment would shrink by 75 percent from 8 percent of the current market

in 2015 to an amount in 2019 which is equivalent to 2 percent of the 2015

market. On the other hand, the oil and gas aftermarket and market for

small projects would remain flat during the four year period. In fact, the

market for pumps for pipelines will be positively impacted as low cost oil and

gas needs to be moved to more places.

The petrochemical market will grow faster at $40 oil. Municipal water and

wastewater will be unaffected by the fluctuation in oil prices. Lower

prices will result in more gasoline being consumed and more oil being refined.

The power market will be impacted by greater use of gas turbine combined cycle

power plants but total revenues for pumps in the power market will not be

impacted greatly by fluctuating oil prices.

McIlvaine will continue to assess the likely changes in oil prices based on the

following factors:

·

The break-even cost for a new well

o

Hydraulic fracturing break-even point is $30 to $50/barrel equivalent based on

improved management practices and the extraction of more product from existing

wells.

o

Oil and tar sands projects break even at $65/barrel.

o

Subsea is more expensive.

·

New technology developments

o

Bechtel experience with coal seam gas to LNG in Australia indicates lower break-

even costs than subsea extraction.

o

China coal to syngas and chemicals could be an alternative which is more than

competitive at $40 oil. McIlvaine has recommended marrying the two stage (HCl/SO2)

scrubbing along with conventional hydrochloric acid leaching to extract rare

earths and generate byproduct revenue.

·

Demand

o

The slowdown in China could impact demand as could economic problems in Greece

and other countries.

o

Demand is a function of industrial activity. There is little equipment

needed to extract Saudi oil. On the other hand, over 2,000 companies rely

on the Alberta oil sands market for their revenues. The greater the industrial

activity the greater the oil demand.

·

Supply

o

Saudi Arabia could choose to restrict production. In many ways the

situation is analogous to the gold in Ft. Knox. You could sell it at any

price and generate positive cash flow. However it is a precious and finite

resource which is important to future generations.

o

Market driven companies will typically be reactive rather than proactive and

will only increase drilling after oil prices rise to a level to make drilling

profitable.

·

Political developments

o

Lifting the Iran embargo on oil exports.

o

Russian activities in the Ukraine and elsewhere.

o

Chinese efforts to manage the economy.

o

Uncertainties in North Korea, Greece and Venezuela.

·

Regulatory initiatives

o

Export restrictions.

o

Climate change regulations.

o

Pollution control requirements for hydraulic fracturing.

·

Traumatic events

o

Major oil spills.

o

Large meteorite impact, earthquake or major volcano eruption.

Some of these developments are more predictable than others. The low oil

prices leads to lower extraction activity which eventually leads to shortages

and higher prices. On the other hand, wars, oil spills and earthquakes

cannot be easily predicted. As a result there will be the need for

continuous changes in the forecasts to take into account the surprises.

Pumps World Markets,

click on:

http://home.mcilvainecompany.com/index.php/markets/2-uncategorised/116-n019

McIlvaine Hot Topic Hours and Recordings

McIlvaine webinars offer the opportunity to view the latest presentations and

join discussions while sitting at your desk. Hot Topic Hours cater to the end

users as well as suppliers while the Market Updates cater to the suppliers and

investors. Since McIlvaine records and provides streaming media access to

these webinars there is a treasure trove of value only a click away. McIlvaine

webinars are free to certain McIlvaine service subscribers. There is a charge

for others. Hot Topic Hours are free to owner/operators. Sponsored

webinars provide insights to particular products and services. They are

free. Recordings can be immediately viewed from the list provided below.

|

DATE |

UPCOMING HOT TOPIC HOUR |

UPCOMING MARKET UPDATES |

|

Sept. 24, 2015 |

Power Plant Water Monitoring |

|

|

Sept. 25, 2015 |

Pump Market Forecast Changes |

|

|

October 1, 2015 |

Power Plant Water Treatment

Chemicals |

|

|

October 2, 2015 |

Fabric Filter Market Forecast

Changes |

|

|

October 22, 2015 |

Precipitator Improvements |

|

|

November 12, 2015 |

Dry Scrubbing |

|

|

December 3, 2015 |

NOx Reduction |

----------

You can register for our free McIlvaine Newsletters at:

http://home.mcilvainecompany.com/index.php?option=com_rsform&formId=5

Bob McIlvaine

President

847-784-0012 ext 112

rmcilvaine@mcilvainecompany.com

www.mcilvainecompany.com