Modest Growth for Subsea Valves

The demand for subsea valves is increasing due

to the elevated prices of oil and gas. Over the

next few years prices are likely to remain high

due to the world political situation. Increases

in subsea production are underway but one

constraint is the long period between project

start and completion. There are also

uncertainties about the quality and

accessibility of the reserves.

Ukrainian forces recently attacked offshore oil

and gas drilling platforms in the Black Sea.

International valve and other component

suppliers have discontinued service to Russian

oil and gas producers. The embargo on Russian

oil and gas is strongly backed by the EU and

many democratic countries.

Rental rates for offshore oil and gas rigs have

soared, and their availability is one of the

hurdles. New subsea wells require years to

complete. In contrast wells in the Permian basin

in Texas can be completed in months.

The growth in the subsea valve market will be

determined by the comparative cost and

availability of new oil and gas from onshore

reserves.

OPEC+ agreed to boost its monthly production

growth target from 432,000 bpd to 648,000 bpd

recently. But oil prices actually rose. It was

because of lack of spare capacity.

This is due to underinvestment in new oil

exploration, in large part a result of the

investor shift to ESG opportunities and

government policies.

Across OPEC+, there are only a few countries

that can actually boost their oil production.

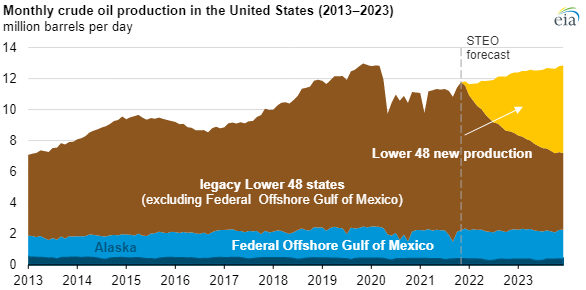

EIA forecasts that crude oil prices will remain

high enough to drive U.S. crude oil production

to record-high levels in 2023, reaching a

forecast 12.6 million barrels per day (b/d). EIA

expects new production in the Permian Basin to

drive overall U.S. crude oil production growth.

EIA expects U.S. crude oil production to

increase to 12.0 million b/d in 2022, up 760,000

b/d from 2021. EIA forecasts crude oil

production to rise by 630,000 b/d in 2023 to

average 12.6 million b/d. More than 80% of that

growth will come from the Lower 48 states

and not from Alaska and the Federal Offshore

Gulf of Mexico.

Production from new Lower 48 wells, particularly

in the Permian region, will drive the forecast

of U.S. crude oil production growth. Legacy

production, or crude oil production from

existing wells, typically declines relatively

quickly in tight oil formations, and EIA expects

that production from new wells will offset these

legacy production declines.

Figure 1

U.S. crude oil production

.

The following factors shape the subsea valve

market

•

CapEx is the leading

indicator of subsea valve spend

•

Major

deep subsea reserves and CapEx are West Africa,

Latin America, and GoM (Brazil, USA, Nigeria,

Angola, Ghana).

•

Development time for subsea investments averages

5 to 8 years, from exploration to first

production.

•

Subsea completions (wet trees) are strongly

favored for ultra-deepwater basins at depths

greater than 5,000 feet for reasons of cost and

technological performance.

For shallower waters, dry trees are

favored for lower cost, direct vertical access,

and established track record.

•

Nearly 85% of subsea CapEx is concentrated in

deepwater and ultra-deepwater basins.

•

Cost curves for ultra-deepwater production are

in the range of $75 to $85/bbl, which is an

approximate proxy for subsea completions.

Cost curves vary by geographic region

reflective of “local content” requirements, as

well as water depth and geologic differences.

•

Key Trends: modularization and standardization

of subsea equipment

•

Key Challenges: cost and lead-time reductions

for subsea equipment

•

Subsea completions are more demanding than

surface completions in terms of depth, pressure,

corrosion, accessibility, reliability

requirements, and other metrics, but experience

has shown that technological solutions have been

developed to meet the challenges.

•

Cost considerations and technological

limitations regarding dry tree technology

strongly favor wet trees for the ultra-deepwater

basins at 5,000 feet and deeper.

•

Primary valves include full-ported gate and

ball.(1)

Butterfly valves with bore obstructions

are not piggable and have limited application in

subsea.

•

Subsea vertical trees may preferentially reflect

usage of gate valves to minimize vertical space

requirements.

•

Subsea horizontal trees may preferentially

reflect usage of ball valves.

•

Both tree types use ½” to 1” small-bore ball

valves for chemical injections, instrument

isolation, etc., with up to 30 valves per tree.

•

Subsea pipelines and manifolds primarily reflect

usage of trunnion-mounted ball valves

The Offshore Technology Conference and

exhibition was held in May. Some 25,000 people

traveled to Houston. The exhibition included

more than 1000 stands of which 100 were

associated

with valves in one way or another.

Many were distributors or suppliers of packages

which included valves. There were less than 10

of the large international valve suppliers with

displays. This indicates the specialized nature

of offshore valve requirements.

As can be seen in figure 1 the valve exhibitors

are from many countries. The large number from

Korea is indicative of government support for

suppliers to the energy industry. Korea had a

pavilion at PowerGen held in Texas in May.

|

Company |

Location |

Valve Type |

|

4E Valve |

TX |

Globe, Check, Ball, Butterfly valves |

|

Asahi |

MA |

Plastic Valve assemblies |

|

BREDA ENERGIA |

Italy |

High pressure valves and Christmas trees |

|

D-Lok |

Korea |

Ball, needle, check valves |

|

Dongsan |

Korea |

Steel valves |

|

Frontier |

Canada |

Ball valves, pig valves, inline chokes, |

|

HanSun |

Korea |

Valves up to 64” |

|

IMI PBM |

PA |

Valves for ballast water and injection |

|

IVI |

India |

High pressure needle, block and bleed valves |

|

Italbest |

Italy |

Sub-sea ball valves |

|

Oxford Flow |

UK |

Stemless actuated valves |

|

PDC Valve |

PA |

Butterfly valves and actuators |

|

Petrolvalves |

Italy |

Turbine bypass valves |

|

PK Valves |

Korea |

Valves and services |

|

RR Valves |

TX |

Reset relief valves |

|

SI Flow Tech |

Korea |

Plug and check valves |

|

Shipham |

UK |

Valves for corrosive media |

|

VALVITALIA |

Italy |

Isolation and control valves |

The subsea valve market will continue to be

shaped by several factors. World politics will

be dominant with large supplies from Russia

likely to be unavailable. Another factor is the

potential to increase supplies of less costly

oil. The third factor is ESG. The impact of a

spill in the ocean is compared to environmental

impacts of tar sands with the higher energy

input and pollution in converting contaminated

to purified liquids.

Both the tar sands and subsea are long term

investments and therefore compete for the same

capital whereas shale oil is based on short term

criteria.

(1)

Industrial Valves: World Market

published by the McIlvaine Company.