|

WELCOME

Weekly selected highlights in flow

control, treatment and combustion from the many McIlvaine publications.

· The Opportunistic Antidote to the Climate Change

Doomsday Scenario

·

Urgent Answers for Flow and Treat Suppliers

·

Determining Flow and Treat Market Shares and

Rankings

· U.S. Coal Fired Flow and Treat Market will be

Diminished but Significant

The

Opportunistic Antidote to the Climate Change Doomsday Scenario

The

U.S. Administration will support a trillion tree planting campaign along

with many other nations. However, the U.S. still believes that warming may

be caused by solar activity and that increased CO2 levels are a result and

not cause of the warming. What if the U.S. government officials are wrong

and the doomsday predicters are right?

They say we are reaching a tipping point and it will be difficult if

not impossible to prevent the catastrophic floods and fires without

immediate cessation of fossil fuel burning.

Fossil

fuel elimination will certainly threaten economic prosperity throughout

Asia. If Asian nations are not

participants any reductions in Europe and the U.S. will be insignificant.

The

solution to this dilemma is a Doomsday antidote which is Opportunistic

Biomass Combustion and Sequestration. A UK consortium is already

generating a significant amount of its electricity from biomass burning and

will be distributing CO2 and hydrogen to industrial facilities and

sequestering the remaining CO2 underground.

In Canada the SaskPower Boundary Dam 3 coal fired plant has now

supplied 3 million tons of CO2 for enhanced oil recovery.

So

there is no doubt that biomass combustion and CO2 sequestration is a

legitimate option. The question is

how costly will it be? It will not

be cheap but on the other hand if the doomsday believers are correct then

it could be the only option. This biomass combustion/sequestration will

“suck the CO2 out of the air”. Wind

and solar are just neutral. So the biomass option is the antidote for the

doomsday scenario.

The

greater the impending doom the greater the amount of biomass which should

be grown, combusted and sequestered.

But to be opportunistic why spend the money if it is not

needed. So the opportunistic

approach is to build and retain biomass capable fossil fuel boilers. Should

the coal fired boilers being retired in the U.S. be scrapped or should they

be mothballed and ready for conversion to biomass firing if needed?

Should

utilities reconsider scrapping the coal plants and building natural gas

fired units? Or should they design

natural gas fired plants for eventual biomass gasification and

sequestration?

Should

the Philippines make its new fleet of coal fired boilers biomass ready? It

is a major target of the trillion tree initiative. There needs to be an

optimization of four initiatives

· Tree planting for long term

sequestration (hundred years)

· Biomass fuel growth with the most mass

in the shortest amount of time

· Biomass combustion

· CO2 use and sequestration

Due

to the uncertainties the wise course is to spend modest amounts to make

combustion plants ready for biomass combustion while continuing to develop

new sequestration strategies including substituting CO2 for water in

hydraulic fracturing.

A

biomass capable electricity generator becomes the highest ranking choice

with wind, solar, hydro and other options falling behind. Biomass may never be burned but if the

doomsday scenario becomes part of the strategy then it is the antidote.

Details

on the strategies, projects, and on all coal fired generators around the

world are included Utility Tracking

System. http://home.mcilvainecompany.com/index.php/databases/42ei-utility-tracking-system

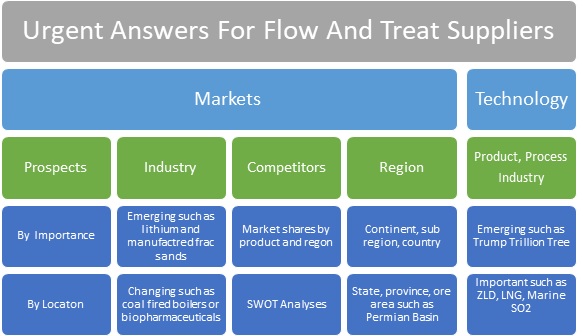

Urgent Answers for Flow and Treat

Suppliers

The

CEO may be evaluating an acquisition and needs a question answered

immediately. The valve salesman

covering BASF may be bidding a large project and want to know which

companies have supplied control valves for condition monitoring. The Asian

sales manager may want to plan his next trip to India so that he visits the

most important prospects. The business development manager may want an

opinion as to the impact of the U.S. endorsement of the trillion tree

program.

These

are all questions which require answers immediately. The McIlvaine Company has nearly 100

services which provide answers to these types of questions. However, they are only available to

subscribers and they take time to search.

An

alternative is the “Urgent Answer” program.

The response can be a phone call, webinar or report. The client does

not have to be a subscriber.

Answers

are available for both market and technology questions. If it is important to know the size of

the market in California or Thailand for valves, pumps, filters,

centrifuges, etc. it is instantly available. If you want to know market share by FGD

scrubber type in India it can be provided.

The

Urgent Answer Program can be expanded to include monthly webinars on

predetermined subjects or speeches at sales meetings.

For

more information on this program contact Bob McIlvaine at 847 784 0013 or rmcilvaine@mcilvainecompany.com

Determining Flow and Treat Market

Shares and Rankings

Flow

and treat suppliers set a high priority on determining the market share for

their products as well as their ranking among competitors. There is

promotional as well as strategic value. The research needed to generate

promotional value is modest. The research needed to maximize the strategic

value is considerable.

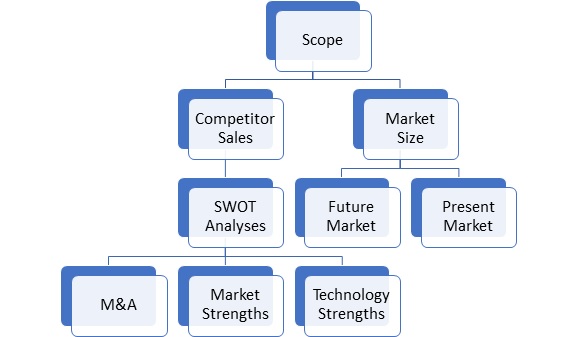

Scope:

To create promotional value it is relatively easy to pick a market

scope which favors the company. To create strategic value, it is desirable

to carefully assess the following definitions

· Product which is being evaluated

· Application

o Industry

o Process

o Medium (gases,

liquids, free flowing solids)

· Geographic scope

· Time frame

· Customers (the largest purchasers with

centralized flow and treat purchasing are larger customers than half the

countries of the world.)

Market Share and Rankings Analysis

Needs

Market Size: The true market size often requires

understanding of the industries, the applications and even the equipment

choices. What percentage of sewage sludge is dewatered in belt filter

presses, centrifuges, or recessed chamber filter presses? If you sell filter cloths or filter belts

this is an important investigation.

Determination

of the future market is very important.

If the supplier can gain market share in an expanding market the

impact on revenues is substantially greater than gaining market share in a

stable or shrinking market.

Competitor

Sales: It is desirable to not only assess the

present sales of the major competitors but also predict their future sales

and market shares. This requires considerable effort but there are multiple

values. McIlvaine analyzes the participation of flow and treat companies in

hundreds of exhibitions around the world.

Some are industry oriented such as ACHEMA. Some are equipment oriented such as Valve

World or FILTXPO. Exhibitions such

as PowerGen are held in Asia, the U.S. and Europe. So, insights on geographical strategy can

also be ascertained.

It

is also desirable to conduct SWOT analyses for major competitors and to

assess their product development activity. The McIlvaine company has

services on air pollution control, water pollution control, combustion,

drying, separation and other processes which provide unique insights on

product development progress and needs.

Market

share is impacted by mergers and acquisitions which are resulting in larger

and larger companies with increasing market share. Suppliers need to keep

analyzing the consequence of a merger among competitors. In some cases,

market ranking may drop but market share will increase. For example, two

smaller competitors could merge but then their combined sales do not reach

the level that they would have reached as independent companies.

With

the broad range of market and technical services offered the McIlvaine

Company is uniquely qualified to assist flow and treat companies with

market share and ranking analysis.

For more information contact Bob McIlvaine at 847 784 0013 or rmcilvaine@mcilvainecompany.com.

U.S. Coal

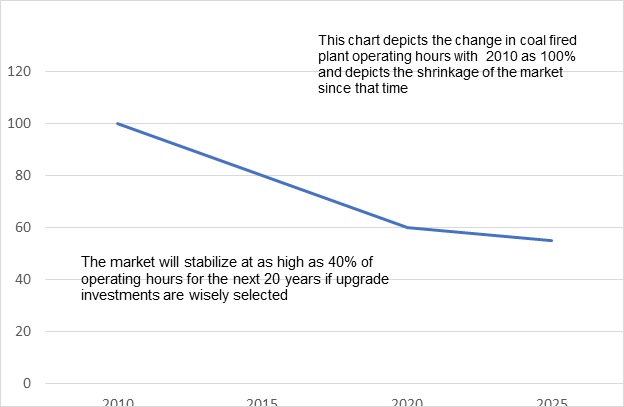

Fired Flow and Treat Market will be Diminished but Significant

Flow

and treat product suppliers should not overlook the U.S coal fired generator

market. It will be significant through 2040. The U.S. coal fired capacity

will shrink to less than 50 percent of the 2010 peak. Operating hours will shrink even further

as coal plants are used in conjunction with solar and wind. However, coal

can maintain a contribution equivalent of 40 percent of that in 2010 if

wise upgrade investments are made.

U.S. Coal Fired Power Operating Hours

as a % of 2010

There

are many uncertainties but the variables which are under control of the

industry are more important than the political variables. The biggest factor affecting coal use in

the U.S will be the price of natural gas which in turn will be closely tied

to world oil prices as LNG plants are built in the U.S. and create a big

gas export market.

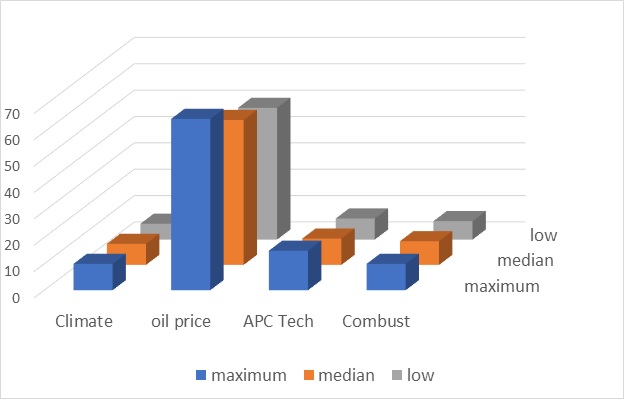

Impact of Factors on U.S. Coal

Megawatt Hours

Assuming

that any movement to prohibit hydraulic fracturing would be rebuffed the

continued low price of oil and gas is highly predictable. As a result, the gas price will be a

large but predictable factor reducing coal use. Climate policy over the

period through 2040 is likely to be a minor factor regardless of whether

there is a Democratic or Republican Congress and Administration. There are

not going to be any new coal fired plants.

There will be continuing pressure to operate existing plants more

efficiently to reduce CO2 and with reduced air pollution.

Investments

in combustion and air pollution control technology will have more impact on

operating hours than will climate change. These investments can make coal

plants more flexible and able to operate more efficiently at reduced loads

and in a cycling mode.

China

is taking the approach of upgrading coal fired plants to make them equal to

gas fired plants in terms of emissions.

This includes upgrades to ultrasupercritical operation. Given an assumption of retirement in 2040

only a minority of U.S. plants will be able to justify this

investment. However, there are many

investments with a high return over just a few years.

Injecting hydrated lime ahead of the

SCR and the air heater can lower the SO3 concentrations enough to avoid

maintenance and turn down issues. Injecting enough sorbent further upstream

in the flue gas means utilities can lower load and capture waste heat that

would typically escape from the stack. This also gives utilities flexibility

to run the coal-fired units at a lower load, typically at night, and be

more efficient. Buckeye Cardinal

Unit 2 in Brilliant Ohio initiated this change in 2017 and is experiencing

a high ROI.

There are many other initiatives which can be

pursued. Here are some.

· Catalytic filters with DSI ahead of

the air heater and capture of heat and water which otherwise is lost

through the stack (ideal where hot precipitators are still being used)

· Byproducts such as rare earth

feedstocks, hydrochloric acid, pure white gypsum to compete with

precipitated calcium carbonate, ammonium sulfate, and sulfuric acid all

have potential for certain site-specific situations

· CO2 as a product: SaskPower supplies CO2 for enhanced oil

recovery from its Boundary Dam plant. BHE in Utah directs CO2 from its gas

turbine stack to a commercial tomato greenhouse on site. Most commercial

greenhouses purchase CO2. Hydraulic fracturing with CO2 is promising as a

way to reduce water consumption and sequester greenhouse gases.

All

of these initiatives and the fate of each coal fired plant is being

analyzed and tracked in the McIlvaine Utility

Tracking System: http://home.mcilvainecompany.com/index.php/databases/42ei-utility-tracking-system

Bob

McIlvaine can answer your questions at 847 784 0013 or rmcilvaine@mcilvainecompany.com

Click here

to un-subscribe from this mailing list

|