|

WELCOME

Weekly selected highlights in flow control, treatment and combustion from the many McIlvaine publications.

- Briefs

- What do Biopharmaceuticals, Shale Fracturing and IIoT have in Common

- Contract Manufacturing Impact on the Combust, Flow, and Treat (CFT) Industry

Briefs

IIoT: Emerson is buying Intelligent Platforms from GE. It is testimony to the rise of Emerson and the descent of GE in the IIoT and Remote O&M market. We cover the development on a monthly basis in the

N031 Industrial IOT and Remote O&M

Fabric Filters: A number of media companies are now supplying filter bags using ceramic fibers. Some are also supplying the bags with embedded catalyst. This technology continues to hold a big potential for coal fired power

N021 World Fabric Filter and Element Market

Midterms: The Democratic gain of control in the U.S. House of Representatives does not augur any immediate reversal of environmental policy. However it does indicate a potential departure of Trump from the scene in 2020 and what could then be a big reversal in policy. Many of the changes in the last two years were easily accomplished. Years of debate and fine tuning of proposed regulations were made irrelevant with one swipe of the pen. The reverse could also be true where one more swipe of the pen restores the regulation as originally promulgated.

What do Biopharmaceuticals, Shale Fracturing and IIoT have in Common

Biopharmaceuticals, shale fracturing, and IIoT are very important to suppliers of combust, flow, and treat (CFT) products and services. Here is what they have in common

· High growth opportunities

· U.S opportunity is very large

· U.S. success can be leveraged internationally.

There is a warning about this unique American opportunity best explained by the question. What do coal fired boiler APC, semiconductor manufacturing, and mobile phones have in common? The answer is that the U.S. is no longer the center of activity and those American companies who did not seize the international opportunity are no longer leaders. The Chinese now are the coal fired boiler APC leaders. TSMC in Taiwan is the leading chip manufacturer. 400 million people in India have mobile phones which relegates the U.S to third place behind China in mobile phone use.

Biopharmaceuticals: The combust, flow and treat revenues for this industry will be growing at more than 10 percent per year. The U.S. is where the action is. Over 40 percent of the market is in the U.S. Filter suppliers such as Pall and Millipore are on the cutting edge of single use technologies. Crane and ITT are leaders in valve development. AES is a leading supplier of turnkey cleanrooms for this industry. Baker is a leader in biosafety cabinets. U.S. companies or U.S divisions of international companies will have the opportunity to expand with the industry as it internationalizes. McIlvaine is conducting a number of webinars on the subject in the first quarter First Quarter 2019 Webinars will Focus on Biopharmaceuticals

Shale fracturing: One can argue that the present booming U.S. economy is primarily the result of a few individuals who innovated fracturing technologies for shale over the last two decades and made the U.S. a world leader in gas and oil production. These innovations continue as U.S. companies have perfected horizontal drilling techniques, proppant design and have found all sorts of ways to make the cost of oil and gas competitive with other sources around the world. This extends to related processes.

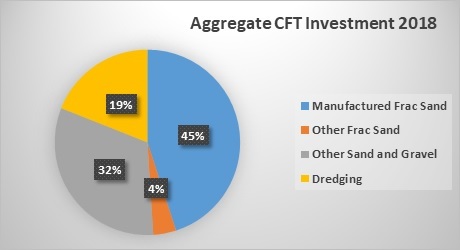

CFT suppliers have big opportunities in the fracking processes and transport and treatment of the products. They also have big opportunities in related processes such as Frac sand. The cost of fracking is being reduced by the use of Texas and local sands rather than the superior natural sands found in Wisconsin. CFT equipment and services are utilizing local sands treated in a series of wet and then dry processes to create equivalent proppants delivered at lower cost. A number of U.S. companies are wet and dry plant design leaders. All of this activity is covered in various market reports http://home.mcilvainecompany.com/index.php/markets. Details on the companies and technology are tracked in N049 Oil, Gas, Shale and Refining Markets and Projects.

However, the opportunity is fleeting. One Japanese supplier has moved into the frac sand plant delivery. Sinopec, one of the world’s largest oil and gas companies has the American Jereh division in Houston and supplies fracking trucks, valves, and pumps. Sinopec has also tailored the fracking technology to make it economical to extract oil and gas in China. China has the world’s largest shale reserves. So the challenge for CFT suppliers will be to create winning strategies for the international market by leveraging the short term advantage in the U.S.

How is this possible? The domination of China in coal fired boiler air pollution control was not inevitable. B&W had thousands of people in its China. All the early FGD systems in China were through international licenses. The problem was that as the licensees embarked on supplying three times as much FGD as had been installed in the U.S. they became the most expert and experienced providers. The solution for B&W and other international suppliers could have been IIoT and Remote O&M. Doosan and MHPS are taking this path to insure their international position. So this leads us to the third commonality.

IIoT and Remote O&M: B&W still retains the experience and knowledgeable people to help coal fired boiler operators around the world. B&W bought the Joy air pollution control group decades ago. This group along with Nitro Atomizer developed spray drier FGD. In 1969 B&W became the second company to supply a wet FGD system and was an early leader in the technology. B&W has a substantial share of the U.S. inventory of FGD plants and also through licensees and joint ventures has worldwide experience. B&W supplies parts and service. With wireless transmission, remote monitoring and data analytics B&W subject matter ultra-experts (SMUEs) can be generating revenues for B&W at coal plants around the world.

GE is in a very good position to capitalize on the coal fired boiler wisdom residing in Connecticut as a result of the ownership of the former CE. It also owns what was once Flakt air pollution control. The legacy companies supplied the first FGD system at Union Electric in 1968 using scrubbers supplied by Environeering. At the time Robert McIlvaine was president of Environeering. CE later licensed the scrubber technology.

The CEO of GE coined the term IIoT and has been a leader in the adoption of this concept in several different industries. U.S. companies are leaders in automation, controls, wireless communication, data analytics and subject matter expertise. A U.S. CFT system supplier can incorporate the latest process management software, and data analytics using products of U.S. based companies with an international reach. This applies not only to coal fired boiler FGD but to biopharmaceutical and semiconductor cleanrooms, ultrapure water, and exhaust gas treatment. A webinar January 9 will cover this opportunity The IIoT Market Size and Structure. The full analysis is described at N031 Industrial IOT and Remote O&M

Bob McIlvaine can answer your questions at rmcilvaine@mcilvainecompany.com 847 784 0012 ext. 122

Contract Manufacturing Impact on the Combust, Flow, and Treat (CFT) Industry

Contract manufacturing is having a significant impact on the CFT industry in two ways

· Some of the largest customers in semiconductors and pharmaceuticals are contract manufacturers

· CFT suppliers are sub-contracting larger percentages of the components, e.g. castings

Semiconductor Contract Manufacturing: McIlvaine editors were too busy at a Semicon West exhibition in San Francisco in the 1980s to take advantage of the opportunity to interview an entrepreneur who had decided to build a foundry in Taiwan. The whole idea of someone other than a semiconductor company building chips seemed strange. In retrospect this was the beginning of the end of U.S. dominance in chip manufacture. Today only a handful of companies have the sales volume to operate as integrated device manufacturers operating their own fabrication facilities. Other chip firms are “fabless” meaning that they design and market semiconductors but contract production to “foundries” that manufacture semiconductors to order. Taiwan Semiconductor Manufacturing Company (TSMC) operates the world’s largest foundry.

The semiconductor production process has three distinct components:

1. Design;

2. Front-end fabrication, in which “fabs” create microscopic electric circuits on silicon wafers

3. Back-end testing, assembly, and packaging, in which wafers are sliced into individual semiconductors, encased in plastic, and put through a quality-control process.

The majority of design work, performed by computer engineers, now occurs in the United States. The designs are then placed on a wafer of silicon or other material in a sequence of more than 250 photographic and chemical processing steps using equipment produced by firms such as Applied Materials, ASML Holdings, and Lam Research. This front-end fabrication process typically takes about two months.

Around 87 percent of advanced worldwide fab capacity is now located outside the United States. Back-end production is where chips are assembled into finished semiconductor components and tested for defects. This stage of the manufacturing process is the most labor-intensive and is often performed in countries such as China and Malaysia, where labor costs are lower than in the United States, Japan, and Europe. The final stage of manufacturing involves the installation of the chips into consumer goods.

Most CFT products and services are used in front end fabrication. So the foundries are large customers. In the 1980s U.S. CFT companies were the world leaders in supply to the semiconductor industry. Today American Air Filter is part of Daikin and has nine manufacturing facilities in Asia. TSMC is now the third largest CFT purchaser in the semiconductor industry.

|

Semiconductor Purchases - $ millions – 2019 - World

|

|

Company

|

Total

|

Intel

|

Samsung

|

TSMC

|

SK Hynix

|

Micron

|

|

Cleanroom

Hardware

|

5500

|

935

|

715

|

605

|

330

|

275

|

|

Cleanroom

Consumables

|

2800

|

476

|

364

|

308

|

168

|

140

|

|

Ultrapure Water Systems

|

900

|

153

|

117

|

99

|

54

|

45

|

|

Scrubbers,

Oxidizers

|

240

|

41

|

31

|

26

|

14

|

12

|

|

Pumps

|

240

|

41

|

31

|

26

|

14

|

12

|

|

Valves

|

400

|

68

|

52

|

44

|

24

|

20

|

|

Cartridges

|

475

|

81

|

62

|

52

|

29

|

24

|

|

Other Filters,

Separators

|

380

|

65

|

49

|

42

|

23

|

19

|

|

Cross Flow

Membranes

|

250

|

43

|

33

|

28

|

15

|

13

|

|

Fans, Compressors

|

290

|

49

|

38

|

32

|

17

|

15

|

|

Treatment Chemicals

|

420

|

71

|

55

|

46

|

25

|

21

|

|

Guide

|

700

|

119

|

91

|

77

|

42

|

35

|

|

Control

|

600

|

102

|

78

|

66

|

36

|

30

|

|

Measure-

Liquids

|

140

|

24

|

18

|

15

|

8

|

7

|

|

Measure-

Gases

|

70

|

12

|

9

|

8

|

4

|

4

|

|

Measure –

Powders

|

40

|

7

|

5

|

4

|

2

|

2

|

|

Other

|

2,000

|

340

|

260

|

220

|

120

|

100

|

|

Total

|

15445

|

2627

|

2008

|

1698

|

925

|

774

|

Pharmaceutical Contract Manufacturing: The global pharmaceutical contract manufacturing market accounts for a little under 10 percent of the total market. Sales were over $90 billion last year. This market is expected to grow at close to 8 percent over the next five years. The percentage of CFT equipment and services purchases to total sales is much higher than for the pharmaceutical companies. So that more than 20 percent of the CFT purchases will soon be made by contract manufacturers.

Owing to the growing demand for generic medicines and biologics, capital-intensive nature of the business, and complex manufacturing requirements, many pharmaceutical companies have identified the potential profitability in contracting with a CMO (contract manufacturing outsourcing) for both clinical and commercial stage manufacturing. Moreover, the pharmaceutical companies have been directing their priorities toward the core areas of competency, and prefer not to use available resources, expertise, and technology on formulating the final dose of medicines. The biggest factor driving the growth of CMOs in the pharmaceutical industry is the growing need for state-of-the-art processes and production technologies, which have proven highly effective in meeting regulatory requirements.

The need for state of the art processes is most critical in biopharmaceuticals which represent 20 percent of the total. McIlvaine is conducting a series of webinars in the first quarter to analyze the biopharmaceutical process evolution First Quarter 2019 Webinars will Focus on Biopharmaceuticals

Among the contract pharmaceutical leaders are

· Catalent

· Patheon

· Baxter

· AbbVie

· Lonza

· Pfizer

· Lonza

· Evonik Degussa

· Royal DSM

· Boehringer Ingelheim

· Fareva

· Aenova

· Famar

· Vetter

· Almac

· Delpharm

· Siegfried

· Corden

· Recipharm

· Aesica

· Nipro

· Daito

· Teva API

· Esteve Quimica

· Euticals

· Zhejiang Hisun Pharmaceuticals

· Zhejiang Huahai Pharmaceuticals

· Shandong Xinhua Pharmaceuticals

· Aurobindo Pharma

· Divis Laboratories

· Dr. Reddy’s Laboratories

Catalent is the world leader in contract manufacturing. It employs over 11,000 people, including over 1,400 scientists, at more than 30 facilities across five continents, and in fiscal 2017 generated over $2 billion in annual revenue.

CFT Subcontracting: Many CFT companies are sub-contracting components, tanks, vessels, and housings. Valve and pump companies are closing down foundries and sub-contracting with Asian foundries for their castings. In China the tons of valves produced soared from 2 million tons to over 10 million tons in just a decade. Formerly most of the valves produced were under sub contract to international suppliers but increasingly China is becoming an exporter of the finished products.

Scrubbers, fabric filters and precipitators consist primarily of steel vessel fabrications. Many are too large to be shipped long distance by rail or truck and need to be fabricated locally. The advantage to international suppliers is that they can supply their products anywhere in the world. The disadvantage is that the ease of fabrication make them vulnerable to local competitors. To preserve their market positon it is necessary to continue to develop new and better products and stay ahead of local fabricators who can only utilizes the existing technology.

Contract manufacturing in several forms will be increasingly important to CFT suppliers. The impact of this trend on markets is covered in the various market reports at http://home.mcilvainecompany.com/index.php/markets

Databases with activity by contract manufacturers is explained at http://home.mcilvainecompany.com/index.php/databases

For more information contact Bob McIlvaine at rmcilvaine@mcilvainecompany.com 847 784 0012 ext. 122.

|