|

WELCOME

Weekly selected highlights in flow control, treatment and combustion from the many McIlvaine publications.

· Valve Market Share Analysis for 140 Companies

· Relevant Pump Market Shares

· MBR Market to Exceed $5 billion in 2024

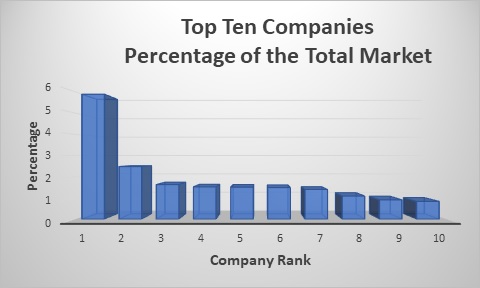

Valve Market Share Analysis for 140 Companies

The McIlvaine market share analysis for each valve supplier is valuable for those companies considering acquisitions, divestiture or seeking to increase share organically. This continually updated database and analysis is part of Industrial Valves: World Markets https://home.mcilvainecompany.com/index.php/markets/water-and-flow/n028-industrial-valves-world-market

There have been a number of mergers, acquisitions, divestitures, and joint venture agreements undertaken by valve companies in the last three years. Emerson has been the most active. The purchase of the valve operations of Pentair (Tyco) the largest valve producer made Emerson the # 1 producer. In the latest 12 months sales are estimated close to $3.8 billion compared to $1.6 billion for # 2 Cameron Schlumberger. The largest divestiture was the GE sale of stock in BHGE to the now independent Baker Hughes with valve sales of $960 million.

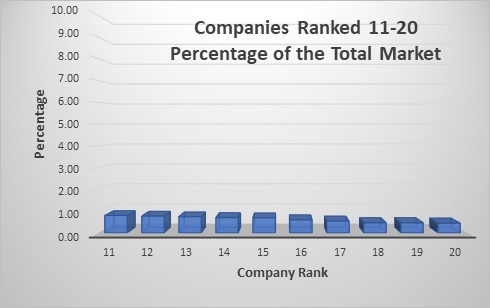

Market shares are being continuously revised to provide worldwide rankings of valve sales by company and further segmented by corporate location.

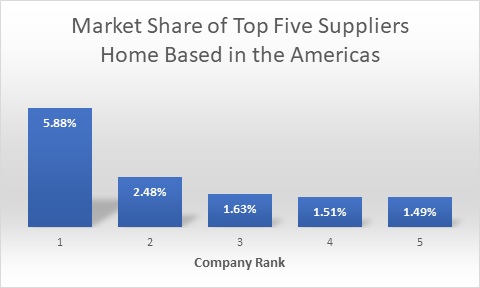

Of the top six ranked suppliers, five are home based in the U.S. Their sales are equal to 15 percent of the world market. There sales equal well over 50 percent of the U.S. market. Their success has come from penetration of the markets in the other two regions.

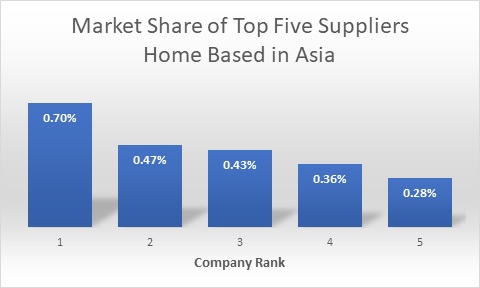

This low percentage reflects the smaller size of the Asian valve companies. However, their growth rate is higher and we can expect these percentages to increase.

Emerson is home based in the U.S. with 2019 valve sales of $3.79 billion its market share on a worldwide basis is over 5%. However, this is equal to18% of the market in the Americas. The fact that Emerson has penetrated the Asian and EMEA markets has allowed the company to grow even if it would be very difficult to achieve an 18% share on the continent in which it resides. On the other hand, Neway has a 0.7% of the total world market. All of its sales represent only 1.6% of the Asian market. It is growing internationally. But even if it were not it still las lots of opportunity in Asia.

Whether a valve company is selling, buying, or seeking organic growth and higher profits, the knowledge of valve company market shares is important.

· Selling: In general, another valve company with synergisms will pay more for a valve supplier than will a private equity investor. This continuing analysis of market shares is a good way to select potential acquirers.

· Buying: The analysis of market shares is very important to valve company acquirers. This analysis should really be just the starting point. Market shares by specific product, process, industry, and location are each significant. While market share for all valves in Asia is part of the report, it is possible to expand this to market share for turbine bypass valves for coal fired power plants in India.

· Organic growth: Sales are not made in a vacuum. Expanding sales means taking share away from some of the existing suppliers. So, a market share analysis is the starting point and also a continuing effort. The competitor share knowledge is important for many throughout the organization including the local salesperson. As competitors merge and gain share it is important to track these changes.

· Higher profits: The # 1 and # 2 suppliers in a given market have the potential for higher profits due to efficient use of resources. Analyzing the profitability of competitors provides insights on how to raise profits. The starting point is market shares.

The market share analysis reviews recent acquisition attempts as well as hedge fund led divestiture attempts to compare the goals of those seeking change to the performance of their targets.

For more information click on Industrial Valves: World Markets https://home.mcilvainecompany.com/index.php/markets/water-and-flow/n028-industrial-valves-world-market

Bob McIlvaine an answer your questions at rmcilvaine@mcilvainecompany.com 847 226 2391

Relevant Pump Market Shares

Management consultants recommend that companies consider market share as a fundamental element of business strategy. The problem is that most market data is unreliable or irrelevant. Knowledge of industries and processes is necessary in order to determine market size. It is desirable to determine market share by pump type but also in each industry and each important market location. Market shares for each major competitor in each niche also should be determined

Pumps: World Markets has market share forecasts for 400 pump companies. It also has purchase forecasts for the largest 100 pump purchasers and 50,000 forecasts of pump markets by industry, country and pump type http://home.mcilvainecompany.com/index.php/markets/water-and-flow/n019-pumps-world-market

This basic report can be expanded to obtain market shares in hundreds of industry sub segments as shown at

http://home.mcilvainecompany.com/index.php/other-services/free-news/news-releases/47-news/1536-nr2542

A much more reliable determination of the market is possible with a market share hierarchy analysis. FGD pumps is an example. Increased GDP is providing the funds to build coal fired power plants in Asia. Many countries in this region are selecting coal as opposed to gas or renewables because of cost and timing.

|

FGD Pump Market Share Hierarchy

|

|

Sequence

|

Choice

|

Alternative

|

|

GDP

|

Power

|

Other

|

|

Power

|

Fossil fuels and waste

|

Hydro, wind, solar

|

|

Fossil fuel

|

Coal and waste

|

Gas turbine

|

|

SO2 removal

|

Incorporated

|

Not utilized

|

|

Absorption

|

Wet

|

Dry

|

|

Wet

|

Limestone

|

Lime, ammonia, MgO

|

|

Design

|

Spray tower

|

Tray tower

|

All these countries are installing flue gas desulfurization systems. Dry systems require only a small investment in pumps. Wet systems require a big investment. Other process decisions also impact the market. It is necessary to understand the processes and predict which will be used. The market for FGD pumps was determined by this method.

|

FGD Pump Market 2021 $ millions

|

|

Total Pump

|

60,000

|

|

Power

|

4,000

|

|

Fossil

|

3200

|

|

Coal

|

3,000

|

|

SO2

|

350

|

|

Wet

|

320

|

|

Wet limestone

|

300

|

|

· New

|

130

|

|

o spray tower

|

110

|

|

o tray tower

|

20

|

|

· Replace, repair

|

170

|

|

o spray tower

|

155

|

|

o tray tower

|

15

|

There are differences in the pump requirement depending on the reagent and the design of the absorber. A tray tower relies on fan energy for mass transfer. A spray tower relies on twice as much slurry for the same result but with lower fan energy. The preference is for spray towers. However, McIlvaine predicts that tray towers will gain market share over the next five years.

Both types require the same amount of limestone slurry feed. However, Chinese plants opt for regional dry grinding rather than purchase of ball mills for wet grinding at the plant.

Most plants use forced oxidation and make wall board quality gypsum. Natural oxidation results in a very difficult sludge which may require reciprocating pumps as the slurry is mixed with lime to make a landfill product.

Market Shares of pump companies for this application are impacted by the choice of absorber, method of grinding, and other process choices.

|

FGD Pump Market Shares

|

|

Type of Process

|

Process option A

|

Process option B

|

|

Absorber

|

Spray Tower

|

Tray Tower

|

|

Absorber recycle pump with up to 500,000 gpm for set of pumps for 1000 MW plant and 98% efficiency. Tray towers require only 50% of the slurry recycle

|

Trillium, KSB, Duechting, and 3 Chinese companies who can supply pumps to handle 50,000 gpm with largest now 80,000 gpm

|

The companies with 50,000 gpm pumps plus the those with flows up to 25,000 gpm such as ITT and many others who also supply dredging and mining pumps

|

|

Grinding

|

Regional Dry Grinding

|

Ball Mill

|

|

Limestone slurry

|

No transport pumps

|

Pumps to transport slurry from the ball mill to the absorber

|

|

Oxidation

|

Forced

|

Natural

|

|

Transport pumps for slurry

|

Centrifugal at modest cost

|

Reciprocating and higher cost

|

The market shares of the pump companies provided in Pumps: World Markets can be expanded to include each relevant niche and to include hundreds of additional competitors beyond the 400 listed.

It is important to determine market shares in niches such as plastic lined pumps for chemical and fertilizer applications, pumps for fruit juices, biopharmaceuticals, lithium mining, and sewage sludge transfer in municipal wastewater plants.

It is also desirable to analyze market share from the process perspective. Some pump companies are involved in the steam cycle with boiler feed water and condensate pumps. Others are involved just with the water intakes and wastewater for those plants. Others are involved in processes involving fluids and slurry e.g. fracking, crude oil.

|

Industry

|

Process

|

Supplier

|

|

F

|

S

|

X

|

IT

|

U

|

I

|

G

|

B

|

5

|

|

Oil & Gas

|

Artificial Lift or Fracking

|

0%

|

0%

|

0%

|

0%

|

0%

|

0%

|

5%

|

26

|

13%

|

|

Refinery

|

Intake

|

5%

|

1%

|

12%

|

4%

|

0%

|

0%

|

0%

|

0%

|

0%

|

|

Refinery

|

Steam

|

8%

|

0%

|

1%

|

0%

|

1%

|

0%

|

0%

|

4

|

0%

|

|

Refinery

|

Process

|

8%

|

3%

|

1%

|

8%

|

3%

|

1%

|

0%

|

3

|

0%

|

|

Refinery

|

Wastewater

|

5%

|

3%

|

12%

|

4%

|

1%

|

0%

|

0%

|

3

|

0%

|

|

Petrochemical

|

Intake

|

5%

|

1%

|

12%

|

4%

|

0%

|

0%

|

0%

|

0%

|

0%

|

|

Petrochemical

|

Steam

|

8%

|

0%

|

1%

|

0%

|

1%

|

0%

|

0%

|

4%

|

0%

|

|

Petrochemical

|

Process

|

8%

|

3%

|

1%

|

8%

|

3%

|

1%

|

0%

|

3

|

0%

|

|

Petrochemical

|

Wastewater

|

5%

|

3%

|

12%

|

4%

|

1%

|

0%

|

0%

|

3

|

0%

|

Analysis by pump type can include designs where there are only 10-20 suppliers such as hydraulically balanced diaphragm pumps, designs such as external gear pumps with hundreds of suppliers or centrifugal pumps with thousands of suppliers.

|

External Gear Pump Market Shares

83 companies analyzed

|

|

Pump Company

|

Total Corporation Pump Sales, Mil $/Yr

|

% of Total Pump Sales

|

External Gear Pump Sales, Mil $/Yr

|

% of External Gear Pump Sales

%

|

Major Applications for EGP

|

|

AB

|

$6.0

|

0.010

|

$1.0

|

0.156

|

Machinery Lubrication

|

|

AL

|

$16.0

|

0.026

|

$9.0

|

1.406

|

Machinery Lubrication

|

|

ALC

|

$6.0

|

0.010

|

$1.0

|

0.156

|

Machinery Lubrication

|

|

AS

|

$1.5

|

0.002

|

$1.0

|

0.156

|

Machinery Lubrication

|

|

B

|

$45.0

|

0.075

|

$3.0

|

0.469

|

General

|

|

Bos

|

$18.0

|

0.030

|

$7.0

|

1.094

|

General

|

|

Bow

|

$6.0

|

0.010

|

$6.0

|

0.937

|

General

|

|

CA

|

$50.0

|

0.083

|

$4.0

|

0.625

|

Machinery Lubrication

|

|

Co

|

$640.0

|

1.060

|

$50.0

|

7.812

|

Machinery Lubrication & Fuel Transfer

|

|

Cor

|

$1.0

|

0.002

|

$1.0

|

0.156

|

General

|

|

Cu

|

$2.0

|

0.003

|

$2.0

|

0.312

|

General

|

|

DEL

|

$20.0

|

0.033

|

$10.0

|

1.562

|

General

|

|

DELT

|

$5.0

|

.008

|

$2.0

|

0.312

|

Machinery Lubrication & Fuel Transfer

|

|

DO

|

$19.0

|

0.032

|

$3.0

|

0.469

|

General

|

Pumps: World Markets has the 50,000 basic forecasts to which customized analyzes can be easily added http://home.mcilvainecompany.com/index.php/markets/water-and-flow/n019-pumps-world-market . Bob Mcilvaine can answer your questions at rmcilvaine@mcilvainecompany.com Direct 847 784 0012 cell 847 226 2391

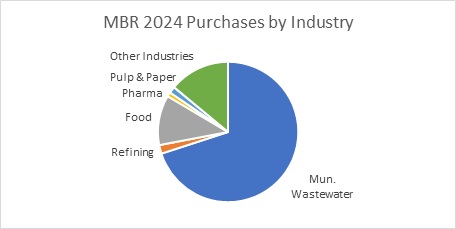

MBR Market to Exceed $5 billion in 2024

The market for membrane bioreactor systems will exceed $5 billion in 2024 with more than $3 billion accounted for by wastewater treatment. This is the new forecast by the Mcilvaine Company in http://home.mcilvainecompany.com/index.php/markets/water-and-flow/n020-ro-uf-mf-world-market.

This material is being added as a separate segment of the RO/UF/MF service due to the large size of the microfiltration and ultrafiltraton revenues associated with this application. The forecast is unique in that the revenues represent the aggregate of what would be reported in financial statements by suppliers. This approach is preferred because

· It is the only way to iterate hard numbers with statistical determinations

· It reflects the revenues of the companies pursuing the MBR market

It includes revenues of suppliers such as Suez and Beijing Origin but just for their initial contract and not for operation revenues. In cases where the MBR is an upgrade to existing biological treatment, the upgrade portion is reflected. In some recent contracts the upgrade value was only 50% of a greenfield complete system.

In cases where there is no identifiable MBR system contractor only the revenues for the MBR components are included. If the broader definition of MBR installed cost were to be the criteria the market in 2024 would exceed $7 billion.

The report includes detailed analysis of system suppliers. In the coming months market shares for membrane suppliers will also be added to the report.

For more information contact Bob McIlvaine at 847 226 2391

|